Volatile energy markets drive prices – gas supply remains stable

At the same time, the physical supply situation remains stable: gas continues to flow via existing import and transit routes and has been moving into storage since the beginning of April. Furthermore, most end customers have fixed-rate tariffs with their utilities and are not affected by global market fluctuations.

Developments in the Middle East and the current disruption of the Strait of Hormuz as a vital LNG trading route have tangibly influenced global energy markets in recent weeks. As seen during previous geopolitical tensions, energy markets react very swiftly to uncertainty, which translates directly into price increases. At the same time, the physical supply situation remains stable: gas continues to flow via existing import and transit routes and has been moving into storage since the beginning of April. Furthermore, most end customers have fixed-rate tariffs with their utilities and are not affected by global market fluctuations.

Austria as a hub in the European gas grid

Austria is part of the European integrated gas grid and serves an important transit and hub function within it. Of particular relevance are transports via the West-Austria-Gasleitung (WAG), which brings pipeline gas from Norway as well as LNG volumes from terminals in Northwestern Europe through Germany to Austria and into neighboring countries to the east. Additionally, in 2025, approximately 10% of imports were delivered from Italy via the Trans-Austria-Gasleitung (TAG).

Gas infrastructure in Europe: available, interconnected, and utilized

Compared to 2022, Europe today possesses significantly expanded LNG import capacities. This has created additional access to global gas markets and increased the flexibility of the European supply system. Whether and to what extent these capacities are utilized depends largely on the global availability of LNG as well as the respective market and price conditions.

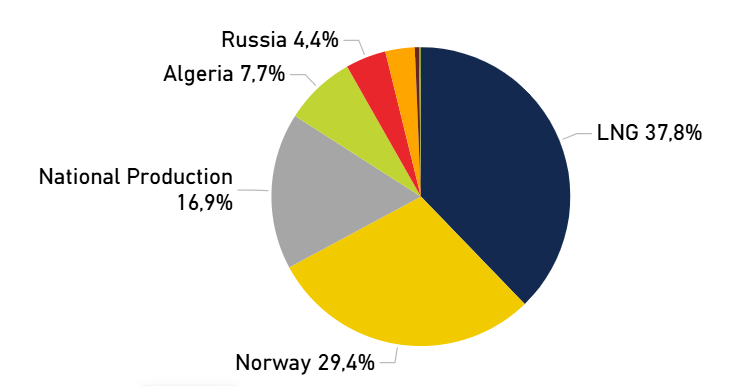

In the 2025 summer half-year, according to the "ENTSOG Summer Supply Review 2025," pipeline gas accounted for around 45% of the European gas supply, with Norway remaining the largest single supplier. During this period, LNG also made a substantial contribution to Europe's supply with a share of around 38%. According to the International Energy Agency ("Gas 2025 – Analysis and Forecasts to 2030"), other key pipeline gas sources notably include Algeria and Azerbaijan.

Gas infrastructure in Europe: available, interconnected, and utilized

Compared to 2022, Europe today possesses significantly expanded LNG import capacities. This has created additional access to global gas markets and increased the flexibility of the European supply system. Whether and to what extent these capacities are utilized depends largely on the global availability of LNG as well as the respective market and price conditions.

In the 2025 summer half-year, according to the "ENTSOG Summer Supply Review 2025," pipeline gas accounted for around 45% of the European gas supply, with Norway remaining the largest single supplier. During this period, LNG also made a substantial contribution to Europe's supply with a share of around 38%. According to the International Energy Agency ("Gas 2025 – Analysis and Forecasts to 2030"), other key pipeline gas sources notably include Algeria and Azerbaijan.

Source: ENTSOG Supply Mix Summer 2025

Storage

The summer injection period began across Europe at the beginning of April. In 2026, storage facilities started with filling levels approximately 18% lower than the previous year, yet they remain within the range of long-term pre-crisis levels. At the European level, the storage level at the beginning of April 2026 was around 28% (approx. 314 TWh) – in Austria at the same time, it was around 35% or approximately 36 TWh, which is above the EU average. In total, Austria has around 100 TWh of storage capacity available. Of this, 20 TWh is allocated to the federal strategic gas reserve.

Austrian gas consumption in 2025 was around 81 TWh (9% higher than the previous year), with more than two-thirds of the demand occurring during the heating period from October to March. During the coldest winter months, approximately 10 to 12 TWh of gas are consumed. The strategic gas reserve thus corresponds roughly to the demand of two cold winter months in Austria. The importance of strategic precautionary measures is also emphasized at the state level: the Ministry of Economic Affairs is currently preparing a gas security of supply package, which includes the extension of the strategic gas reserve.

The ENTSOG Summer Supply Outlook 2026 shows that the European gas system is sufficiently flexible to fill storage facilities before the upcoming heating season. A prerequisite for this is the early and steady utilization of infrastructure – particularly LNG import capacities and transmission pipelines. However, the actual course of storage injection will be largely determined by market and price developments. In scenario analyses, ENTSOG points out that under unfavorable conditions, regional constraints are possible, particularly in West-East corridors and parts of the CEE region. With the construction of the WAG Loop 1, Gas Connect Austria is exactly on the right track to be able to transport more gas into the region.

The European association of gas infrastructure operators, GIE, also points out in its study "Securing Future Supply" from March 2026 that storage facilities fulfill a central insurance and flexibility function in the energy system – not only for gas supply but also for power supply, for instance through flexibly deployable gas-fired power plants.

Context: Infrastructure creates room for maneuver Current geopolitical developments are leading to increased uncertainty and price volatility in energy markets. At the same time, it is evident that the European gas infrastructure, as an integrated system of LNG connections, transmission networks, and storage, is robust, high-performing, and designed for flexibility.

Especially in a volatile geopolitical environment, gas remains a reliable component of the energy supply – thanks to long-term planning, European interconnection and cooperation, and the reliable operation of gas infrastructure.